April's results serve as a powerful reminder that markets are capable of staging impressive recoveries even when investor concerns remain elevated. Despite an ongoing conflict in the Middle East, major equity indices surged to new all-time highs during the month. The S&P 500 posted a gain of 10.4% in April alone, representing one of the strongest single-month performances in the index's history. At a high level, this mirrors the tariff-driven volatility and subsequent recovery seen in early 2025.

That said, this performance should not be interpreted as a signal that smooth sailing lies ahead. Geopolitical tensions, an upcoming leadership transition at the Federal Reserve, and elevated energy prices are all likely to generate significant headlines in the coming months. What April's performance reinforces is that regardless of how difficult the environment may appear, maintaining a well-constructed portfolio that is aligned with long-term financial goals remains the most prudent approach.

Key Market and Economic Drivers in April

• The S&P 500 and Nasdaq gained 10.4% and 15.3% for the month, both ending at new all-time highs, while the Dow Jones Industrial Average rose 7.1%.

• Volatility declined over the month, as measured by the CBOE VIX index, falling from 25.3 to 16.9 alongside improving market conditions.

• International developed markets returned 7.0% based on the MSCI EAFE Index in U.S. dollar terms, while emerging markets returned 14.5% based on the MSCI EM Index.

• U.S. small cap stocks jumped 12.2% based on the Russell 2000 and mid-cap stocks gained 7.8% based on the S&P MidCap 400.

• The 10-year Treasury yield ended the month with little change at 4.37%. The Bloomberg U.S. Aggregate Bond Index was flat with only a 0.1% increase during the month.

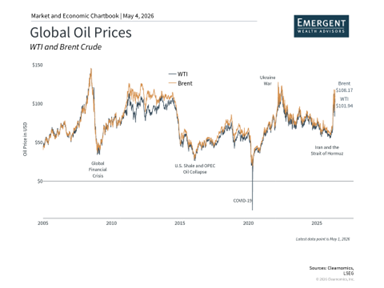

• Brent crude oil ended April at $114 per barrel, with swings from as low as $92 to as high as $121. WTI closed the month at $105, as the Strait of Hormuz remained closed to shipping.

• Gold ended the month at $4,610 per ounce, a slight decline over the month. The U.S. Dollar Index stood at 98.1, down from 99.96 the previous month.

The equity market rebound in context

April's market gains may appear surprising given the prevailing backdrop of geopolitical tensions and policy uncertainty. However, history consistently demonstrates that some of the most powerful monthly market rallies have taken place precisely when investor sentiment was at its most pessimistic. This pattern has emerged across numerous market cycles, including the recovery following the pandemic shock of 2020, the rebound after the inflation-driven bear market of 2022, and the turnaround after the tariff-related pullback in early 2025. While such recoveries are never a certainty, they have a tendency to arrive when they are least anticipated.

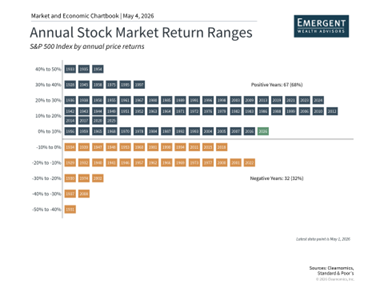

When factoring in the negative returns from the first quarter, the S&P 500 now stands 5.3% higher year-to-date. The accompanying chart illustrates the distribution of annual S&P 500 returns throughout history. Since 1928, the market has delivered positive returns in approximately two-thirds of all years, indicating that while negative years are not uncommon, positive years have been far more frequent over longer time horizons. Since 1980, the share of positive years rises even further, to roughly three-quarters.

This is not meant to suggest that markets always recover swiftly, but rather to highlight the inherent difficulty of attempting to time the market. The experience of recent years provides valuable lessons for investors to carry forward into future periods of volatility, which will inevitably arise.

Jerome Powell's final meeting as Federal Reserve Chair

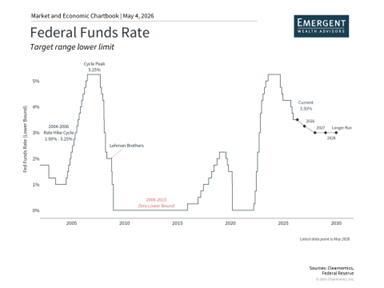

At its April meeting, the Federal Reserve opted to hold its benchmark policy rate steady within a range of 3.50% to 3.75%. Although the decision itself was broadly expected, the level of internal disagreement was notable — four of the twelve voting members dissented, the highest number since 1992. Three of those officials agreed with the rate decision but objected to language in the official statement that suggested future rate cuts remained on the table. One governor advocated for an immediate reduction, consistent with the position that official has taken at every prior meeting attended.

This internal division reflects both a pending leadership change and two distinct economic challenges that the Fed must simultaneously navigate. On the labor market front, conditions have been showing signs of softening, with job openings declining below the number of unemployed workers for the first time in years. On the inflation front, however, the ongoing conflict involving Iran and the continued disruption around the Strait of Hormuz have pushed oil prices higher, feeding through to gasoline prices and broader inflation measures.

Ordinarily, a weakening labor market would argue for rate cuts, while rising inflation would call for rate hikes. As a result, market expectations for the Fed's next move have shifted, with roughly equal odds now being assigned to a rate cut and a rate hike later this year.

April also marked Jerome Powell's final press conference in his role as Fed Chair. He assumed the position in 2018, succeeding Janet Yellen, and has served on the Board of Governors since 2012. Kevin Warsh is expected to be his successor, with the Senate Banking Committee having already approved his nomination. Powell indicated at the press conference that he will remain on the Fed's Board of Governors until ongoing legal actions from the Justice Department are resolved, and expressed his intention to conduct himself in a manner that is respectful of the incoming Chair.

While a change in Fed leadership introduces additional uncertainty regarding the future direction of monetary policy, it is worth noting that both markets and the broader economy have historically performed well across many different Fed Chairs and a wide range of policy environments. A well-diversified portfolio is built to navigate precisely this type of policy uncertainty.

Oil prices and the impact of the Strait of Hormuz closure

Oil prices represent one of the most immediate ways in which the conflict involving Iran is affecting both everyday investors and consumers. Brent crude and WTI prices moved back toward recent highs in April as the Strait of Hormuz remained effectively closed to oil tanker traffic. Throughout the month, a series of false starts around ceasefire discussions and peace negotiations contributed to sharp swings in energy markets.

Despite elevated oil prices, equity markets continued to perform well. The more pressing concern for investors is whether persistently high energy costs will begin to ripple through to other areas of the economy. This "second-order effect" would materialize if oil and gasoline prices remain elevated for an extended period, driving up transportation and energy input costs for businesses, which would then be passed on to consumers in the form of higher prices for goods and services.

That said, some historical perspective is warranted. Past oil price shocks suggest that inflationary pressures can dissipate once the underlying situation stabilizes. The surge in U.S. gasoline prices above $5 per gallon in 2022 ultimately proved temporary as supply conditions improved, even though it created real difficulties for household budgets in the interim. It is also worth noting that the United States remains the world's largest producer of oil and natural gas, which provides a degree of insulation from global supply disruptions that was not available in prior decades.

For investors, this year also highlights the valuable contributions that different market segments can make to a balanced portfolio. Technology-oriented sectors, for instance, performed strongly over the past month, while the energy sector has been a positive contributor to returns this year. Maintaining broad exposure across all parts of the market continues to be an important element of a well-structured investment approach.

The bottom line? April's market rebound illustrates that meaningful gains can materialize even during challenging and uncertain times. A well-constructed portfolio, carefully aligned with your long-term financial goals, is designed specifically to help navigate through these kinds of environments.

Emergent Wealth Advisors provides comprehensive financial planning and wealth management services designed to help clients navigate important financial decisions with confidence. Their team works closely with individuals and families to develop customized strategies that may include investment management, retirement planning, and long-term financial planning. By focusing on each client’s personal goals and financial priorities, they help create a strategic plan to build wealth, preserve assets, and plan for the future. For additional details about the services offered by Emergent Wealth Advisors, please click here. If you are in the Nashville area, click here.