The ongoing conflict between the United States and Iran continues to shift, with financial markets responding to each new development. An initial ceasefire announcement temporarily reduced tensions and drove oil prices lower, with Brent crude declining into the $90 range. However, the subsequent collapse of peace negotiations pushed prices back above $100 per barrel, underscoring how rapidly the geopolitical landscape can shift. While the situation remains fluid, the most critical question for long-term investors is how these developments influence the broader economy, businesses, and consumers.

In practice, geopolitical conflicts tend to affect financial markets primarily through energy prices, which have a direct impact on fuel costs and can then ripple across the economy. The extent to which this affects prices broadly depends on how long energy costs remain elevated. Understanding these dynamics can help investors keep perspective. In particular, inflation, labor market conditions, and corporate earnings offer valuable insights in the current market environment.

Overall inflation is being pushed higher by rising energy costs

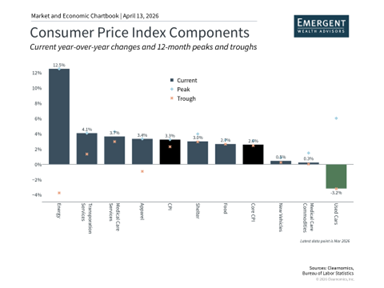

The most immediate way consumers are feeling the impact of the Iran conflict is through higher energy prices. The March Consumer Price Index report revealed that energy costs climbed 12.5% year-over-year, with gasoline prices surging 18.9% and fuel oil rising 44.2%. These increases pushed headline CPI to 3.3%, a sharp acceleration that has understandably raised concerns about a return to the inflation environment seen in 2022. Much of this increase was anticipated, given that the conflict in Iran began at the end of February.

Importantly, the CPI report also indicates that higher energy costs have not yet spread to other key consumer categories. Core CPI, which excludes food and energy, rose only 2.6% year-over-year, coming in below consensus expectations and only slightly above the prior month's reading of 2.5%. An even narrower measure that also strips out housing costs — sometimes referred to as "supercore" inflation — rose only 2.3%.

These figures indicate that while energy costs are reaching consumer wallets — with gasoline averaging $4.12 per gallon nationally, and considerably higher in many areas — these pressures have not yet spread broadly across the economy. This distinction is significant because the primary economic concern is that if oil prices remain elevated over an extended period, higher energy, transportation, and manufacturing costs could filter into the broader prices of goods and services.

Without minimizing the burden that higher gasoline prices place on households, economists generally view these types of supply-side shocks as temporary. The relative stability of core inflation supports the expectation that once the Middle East situation stabilizes, inflation may return to pre-conflict levels. The decline in oil prices following the initial ceasefire announcement further reinforces this outlook. However, the pace of that recovery ultimately depends on how the conflict itself evolves, which remains difficult to predict.

Labor market conditions have softened, though demographic factors complicate the analysis

In addition to inflation, the condition of the labor market is another key variable for investors to watch. The most recent employment report offered a positive surprise, with 178,000 new jobs added in March, surpassing expectations of just 65,000. Nevertheless, the prior month was revised sharply lower to a loss of 133,000 jobs — a reminder that these figures can be volatile and subject to meaningful revision.

Taking a broader view, the overall trend has been one of decelerating job creation. Since the beginning of 2025, the economy has averaged only approximately 21,000 new jobs per month, a significant slowdown from the 122,000 monthly average recorded in 2024. Notably, the unemployment rate has not risen materially; it edged down slightly to 4.3% in March. However, this reflects a contracting labor force rather than robust hiring activity.

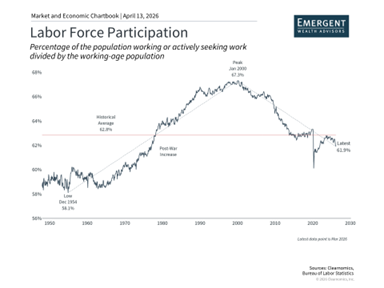

One useful lens for understanding this dynamic is the labor force participation rate, which tracks the share of working-age Americans who are either employed or actively seeking work. As the accompanying chart illustrates, this rate has fallen to just 61.9%, its lowest level since the pandemic. This is not an entirely new development, as labor force participation has been on a gradual decline since the early 2000s, driven largely by demographic factors — most notably, an aging population. For context, more than 11,000 baby boomers are reaching retirement age every single day.

These demographic trends, combined with reduced immigration, mean that a smaller share of working-age Americans is participating in the labor force. This dynamic skews what economists might traditionally consider a healthy labor market. When fewer people are actively participating, the economy requires fewer new jobs each month to sustain low unemployment levels, which can make headline figures more challenging to interpret.

Within the monthly jobs report's details, the picture is similarly uneven. Recent job growth has been concentrated largely in the "Education and Health Services" sector, while the "Information" sector has experienced job losses, consistent with layoff announcements from large technology companies. Wage growth has also moderated to 3.4% year-over-year, though this pace still exceeds the overall inflation rate for many workers, providing some degree of support for consumer spending.

What does this mean for investors? Consumers are grappling with higher costs at a time when labor market conditions are softening. Yet the unemployment rate remains relatively stable, suggesting that those who wish to work are largely finding employment. The key distinction is that a smaller proportion of the overall population is actively participating in the workforce today compared to prior periods.

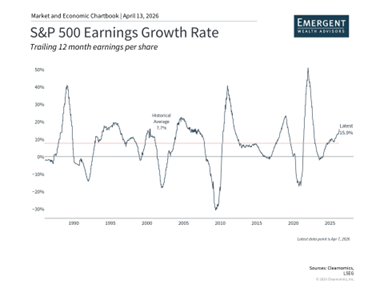

Corporate earnings growth continues to demonstrate resilience

Amid the uncertainty surrounding geopolitics, inflation, and employment conditions, corporate earnings have been a bright spot for investors. Despite the challenges outlined above, consumers have continued to spend, and profit margins have held up well for many companies. Current Wall Street estimates suggest that S&P 500 earnings-per-share have grown approximately 16% over the past twelve months, with expectations for an additional 18% growth over the coming year. These are historically strong figures, well above the long-term average growth rate of 7.7%.

Of course, earnings estimates should always be interpreted with caution, as they are based on analyst projections that can shift as economic conditions change. Tariff policies, elevated energy costs, and a softening labor market could all weigh on profitability in the quarters ahead. Nevertheless, the current trajectory of earnings growth is one reason why stock market valuations have improved recently, alongside the market pullback.

This serves as a reminder that periods of uncertainty, while they may feel uncomfortable, are often when the most attractive opportunities emerge for long-term investors. During bouts of market volatility driven by geopolitical events, earnings expectations frequently hold up better than stock prices. While this does not guarantee a swift market recovery, it does suggest that investors who maintain a long-term perspective and hold well-diversified portfolios are often rewarded for their patience.

The bottom line? Rising energy prices are weighing on the economy at a time when consumers face other headwinds. However, strong earnings growth and more attractive valuations have created meaningful opportunities for long-term investors. Maintaining a diversified portfolio and staying anchored to long-term financial goals remains the most prudent approach to navigating this environment.