The first quarter of 2026 offers a compelling reminder of why preparation is essential in financial planning and investing. Following strong gains in 2025, markets have contended with a combination of geopolitical disruptions, elevated oil prices, and renewed economic uncertainty. The conflict in Iran, which broke out at the end of February, quickly became the defining market narrative, sending oil prices sharply higher and triggering the year’s first notable market pullback. By the close of March, however, reports of a potential ceasefire began to surface, and the situation remains fluid.

Stepping back to view the bigger picture, markets have still delivered impressive performance over the past twelve months. Beneath the headline numbers, several areas of the market — including energy and defensive sectors — have provided meaningful support to diversified portfolios. Looking ahead, new questions are likely to emerge, among them a leadership transition at the Federal Reserve and the midterm election scheduled later this year.

For investors with a long-term horizon, the first quarter serves as a timely reminder that markets rarely follow a straight path, and that the foundations of sound investing are most valuable precisely when uncertainty is at its highest.

Key Market and Economic Highlights

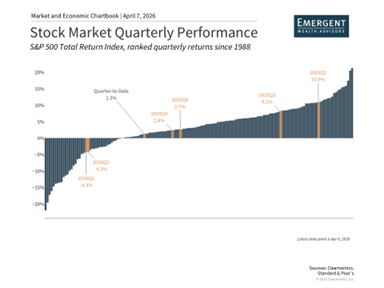

• The S&P 500 posted a total return of -4.3% in Q1, the Nasdaq returned -7.0%, and the Dow Jones Industrial Average returned -3.2%.

• The Bloomberg U.S. Aggregate Bond Index was essentially flat through the first quarter of 2026. The 10-year Treasury yield closed the quarter at 4.3%, having dipped as low as 3.9% at the end of February.

• Developed market international equities (MSCI EAFE) fell -1.1% and emerging market equities (MSCI EM) declined -0.1% over the quarter, both on a total return basis in U.S. dollar terms.

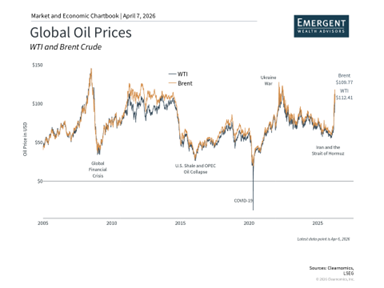

• Oil prices surged, with Brent crude reaching $118 per barrel by the end of March after starting the year below $61. WTI crude closed the quarter at $101 per barrel.

• Gold ended the quarter at $4,668 per ounce, having peaked at $5,417 in January. The U.S. Dollar Index (DXY) edged higher to 99.96 over the same period.

• February inflation data showed headline CPI rising 2.4% year-over-year and core CPI up 2.5%. The core PCE price index, the Federal Reserve’s preferred inflation gauge, rose 3.1% year-over-year in January.

• The Federal Reserve held rates steady within a range of 3.50% to 3.75% at both of its meetings during the first quarter.

The year’s first market pullback arrived in Q1

It is tempting to draw comparisons between the start of 2026 and the opening months of 2025, as both periods were shaped by global concerns. Notably, both first quarters saw the S&P 500 pull back by 4.3%. While last year’s turbulence was driven by tariffs and this year’s by the Middle East conflict, the effect on investor sentiment has been strikingly similar. When uncertainty rises, short-term market swings in response to headlines are a predictable outcome.

Although the past is no guarantee of future results, taking a broader historical view can offer useful context. Despite the headwinds of early 2025, the stock market went on to achieve strong gains throughout the remainder of the year, including numerous record highs across major indices. The lesson is not that markets always rebound swiftly, but rather that market commentary tends to concentrate on negative developments — meaning that recoveries often catch investors off guard.

Perhaps the most grounding perspective is recognizing that pullbacks are a routine and unavoidable feature of investing. Since 1980, the S&P 500 has experienced an average intra-year drawdown of around 15%, even though markets have generated positive annual returns in more than two-thirds of years. It is quite normal for any given year to see four or five pullbacks of five percent or more. Last year saw six such episodes, yet the S&P 500 still finished with an 18% total return.

For investors, the key takeaway is that short-term market swings — especially those fueled by headline risk — are simply part of the investment cycle. Portfolios constructed around long-term financial goals are designed precisely to navigate these moments. This perspective may be especially relevant as the midterm election approaches and fiscal concerns resurface later in the year.

Geopolitics and oil prices remain the central source of market uncertainty

The most consequential market development of the first quarter was the escalating conflict in the Middle East, which pushed oil prices sharply higher. Disruptions to the Strait of Hormuz — a critical chokepoint that carries roughly 20% of global oil from the Persian Gulf to markets around the world — prompted production cuts among major oil-producing nations in the region. Brent crude closed the quarter at $118 per barrel, up more than 94% year-to-date, while WTI crude exceeded $100, the highest levels since the conflict in Ukraine began in 2022. Oil prices will continue to respond to geopolitical developments, including news surrounding a possible ceasefire.

Higher fuel costs affect consumers directly through gasoline prices and indirectly through elevated prices on goods and services throughout the broader economy. The national average price of gasoline reached $4 at the end of March, and diesel prices have also risen considerably.

While these developments do weigh on household budgets, economists generally view such “supply-side shocks” as transitory when assessing the overall health of the economy. This is because oil prices typically stabilize once the underlying geopolitical situation resolves. A comparable dynamic played out in 2022, when gasoline prices climbed to $5 before declining within a matter of months. While the current environment is challenging, significant financial stress is not anticipated for the average American household at prevailing gasoline price levels.

History further demonstrates that geopolitical events, while unsettling in the near term, have rarely derailed markets over the long run. This includes the U.S. operation in Venezuela in January, which caught markets off guard but had limited lasting impact on investments. While the current situation continues to unfold and the humanitarian implications are serious, investors who made sweeping portfolio changes in response to past geopolitical events frequently did so at inopportune moments.

Economic growth is moderating but remains on solid footing

Volatile energy prices represent just one element of a broader economic picture. Other indicators point to an economy that has moderated over the past year but remains fundamentally sound — a notable outcome given that recession forecasts from economists and investors alike have repeatedly failed to materialize in recent years.

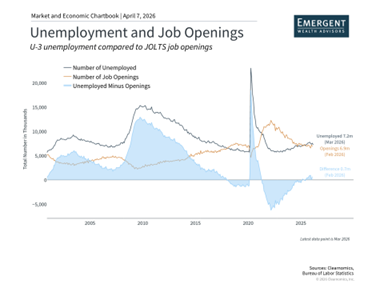

The labor market remains among the most closely watched economic indicators. The latest payrolls data revealed that February job gains fell by 92,000, and the unemployment rate ticked up to 4.4%. Significantly, job seekers now outnumber available job openings for the first time in several years. As recently as 2022, there were two open positions for every unemployed individual, reflecting an unusually tight labor market. That dynamic has now shifted.

Context, however, is important. Fewer workers are entering the labor force due to reduced immigration and an aging population. In other words, both the supply of and demand for labor are easing simultaneously, which has helped keep the unemployment rate near historically low levels. Investors pay close attention to employment data because it has a direct bearing on household income, consumer confidence, and spending. Consumer spending accounts for more than two-thirds of GDP and has remained stronger than many anticipated over recent quarters.

Sector-level performance has varied widely

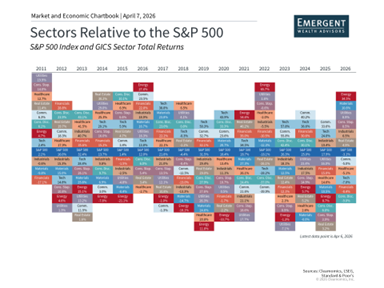

While the overall S&P 500 has pulled back, performance across individual sectors has varied considerably. In fact, six of the eleven S&P 500 sectors have posted positive returns for the year, and the gap between the best and worst performing sectors expanded to nearly 50 percentage points during the first quarter.

The Energy sector has been the standout performer, gaining close to 40% through the end of March, as higher oil prices are expected to lift revenues and attract further investment. Other areas of strength include Consumer Staples, Utilities, Materials, and Industrials, all of which have benefited from a more risk-averse market environment. Many of these sectors are commonly described as “defensive,” given that they represent businesses with relatively stable earnings and cash flows that are less sensitive to the economic cycle.

By contrast, the Information Technology sector has declined approximately 9%, and a number of mega-cap stocks within the Magnificent 7 have underperformed. This represents a meaningful shift from recent years, when a handful of large technology companies accounted for the bulk of market gains.

As always, it is important to keep these moves in proper perspective. As the chart above illustrates, sector leadership is subject to change as market and economic conditions evolve. Energy ranked as the top-performing sector in both 2021 and 2022, a period when technology-related stocks struggled. That pattern then reversed over the subsequent three years. Just as with asset classes more broadly, predicting which sector will lead or lag in any given year is extremely difficult, which underscores the value of a well-diversified portfolio in navigating varied market conditions.

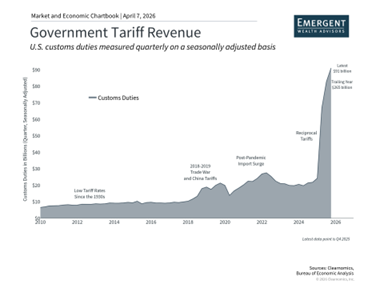

The tariff landscape continues to shift

Trade policy also underwent a notable change at the end of January, when the Supreme Court ruled 6-3 that the broad tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were unlawful. In response, the administration implemented a temporary global import duty under a separate legal authority, Section 122 of the Trade Act of 1974. The administration also launched new Section 301 trade investigations in March, while approximately a dozen Section 232 investigations remain in progress.

For investors, the central takeaway is that while the legal framework underpinning tariffs has changed, the overarching direction of trade policy is expected to continue. Tariffs will likely persist as a factor influencing consumer prices, business costs, and investor sentiment. That said, last year demonstrated that markets can and do adapt to these types of policy developments over time. Regardless of how the tariff landscape evolves in the months ahead, remaining invested and avoiding overreaction to policy shifts remains the prudent course.

The bottom line? The first quarter of 2026 has tested investors with geopolitical shocks, elevated oil prices, and economic uncertainty. Yet markets have demonstrated resilience, and well-balanced portfolios and financial plans have performed the role they were built for. Investors are best served by maintaining their focus on long-term objectives in the months ahead.

Emergent Wealth Advisors delivers customized financial planning and wealth management services for individuals and families seeking a thoughtful, long-term financial strategy. Their team provides support with investment portfolio management, retirement planning, and broader financial planning designed around each client’s goals and priorities. By taking a strategic and personalized approach, they help clients manage risk, grow their wealth, and plan confidently for the future. Discover more about how Emergent Wealth Advisors helps clients plan for the future by clicking here. If you are located in the Nashville area, click here.