February served as a reminder to investors that market progress is rarely linear. After a strong start to the year that carried major indices to record highs, sentiment shifted as a landmark Supreme Court ruling on tariffs, concerns about artificial intelligence, softer labor market data, and significant escalations in the Middle East weighed on U.S. equities. At the same time, international stocks and small caps continued to post strong gains, and bonds advanced further, underscoring the value of maintaining a well-balanced portfolio.

While news-driven events can spark short-term volatility, the broader economy continues to expand and corporate earnings remain on a growth trajectory. Rather than reacting to individual headlines, investors are best positioned by staying committed to a diversified portfolio aligned with their long-term financial objectives.

Key Market and Economic Drivers in February

• The S&P 500 fell -0.9% and the Nasdaq Composite dropped -3.4% for the month. Meanwhile, the Dow Jones Industrial Average rose 0.2%.

• The CBOE VIX volatility index increased to 19.9 at the end of the month due to AI-related concerns and trade policy uncertainty.

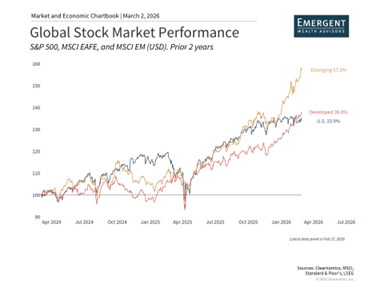

• International developed markets jumped 4.5% based on the MSCI EAFE Index in US dollar terms, while emerging markets gained 5.4% based on the MSCI EM Index. Year-to-date, they have gained 9.9% and 14.6%, respectively.

• U.S. small cap stocks gained 0.7% based on the Russell 2000.

• The 10-year Treasury yield ended the month lower at 3.95%. This is the first month it has fallen below 4% since last November. The Bloomberg Aggregate Bond Index rose 1.6%.

• Gold closed lower at $5,279 per ounce but reached as low as $4,661 at the beginning of the month. Silver ended lower at $93.79 per month.

• The U.S. dollar index rose slightly to 97.6.

• January inflation showed headline CPI at 2.4% year-over-year and core CPI at 2.5%, while the core PCE price index rose 0.4% month-over-month, the sharpest increase in a year.

• The unemployment rate edged down to 4.3% in January, with 130,000 nonfarm payroll jobs added. However, annual benchmark revisions showed the economy created only 181,000 jobs in all of 2025, roughly 15,000 per month.

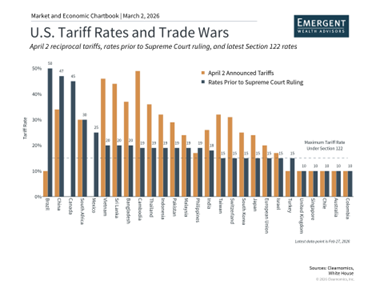

• On February 20, the Supreme Court ruled against the administration’s use of IEEPA-based reciprocal tariffs, prompting a pivot to alternative trade laws.

• On February 28, the U.S. and Israel launched military strikes against Iran, including the compound of Iran’s Supreme Leader who has been reported killed.

How a Supreme Court ruling reshaped trade policy

The most consequential policy event in February was the Supreme Court’s February 20 decision striking down the administration’s tariffs. These had originally been implemented under the International Emergency Economic Powers Act (IEEPA) as a basis for imposing reciprocal tariffs on most trading partners. The ruling carries wide-ranging implications, including the possibility of refunds to businesses and consumers.

In response to the ruling, the White House moved quickly to reestablish tariffs under Section 122 of the Trade Act of 1974, which permits the president to levy tariffs of up to 15% for a period of 150 days. These revised import duties took effect on February 24. The administration is also anticipated to pursue additional measures, including Section 301 of the Trade Act of 1974 targeting unfair trade practices and Section 232 of the Trade Expansion Act of 1962 addressing national security considerations.

For investors, the critical takeaway is that while the legal basis for tariffs has changed, the overall policy direction remains intact. Trade-related uncertainty is likely to continue generating headlines and contributing to market volatility. That said, history suggests that markets tend to adapt to evolving trade conditions over time, particularly as companies adjust their supply chains and pricing strategies accordingly.

Treasury yields reflected some of this uncertainty, with the 10-year yield briefly dipping below 4% for the first time since November. This dynamic provided a tailwind for fixed income portfolios in February and serves as a reminder of the stabilizing role that bonds can play in a balanced investment strategy.

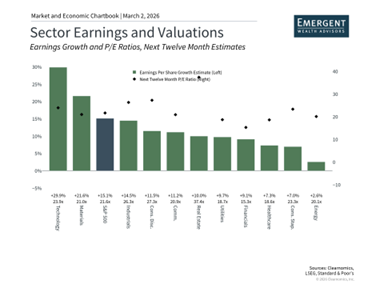

Weighing AI enthusiasm against valuation concerns

Artificial intelligence remained a central theme in market discussions throughout February, though the narrative evolved from concerns about elevated valuations toward a broader debate about the speed and extent of AI-driven disruption to existing business models. Some investors have grown concerned that AI agents could compress software margins, accelerate automation-driven white-collar displacement, and upend traditional industries more rapidly than anticipated.

These concerns have fueled a notable rotation in the market. Investors have been moving away from mega-cap technology names and into sectors considered more resilient to disruption, such as energy, materials, and industrials. This shift—sometimes characterized as a preference for "heavy assets, low obsolescence" (HALO) companies—helps explain why the Nasdaq lagged while other areas of the market advanced.

Although market volatility can be unsettling, this rotation represents a constructive development for long-term investors who have expressed concern about stretched equity valuations in recent years.

Economic growth moderated while labor market signals were mixed

According to the Bureau of Economic Analysis, real GDP grew at an annualized rate of 1.4% in the fourth quarter of 2025, a notable deceleration from 4.4% in the prior quarter and below market expectations of 2.5%. The slowdown was partly attributable to the record-long government shutdown and a pullback in consumer spending. However, business investment expanded 3.7% on an annualized basis, driven by record-setting outlays for AI data centers. For all of 2025, real GDP grew 2.2%, a pace that remains healthy by historical standards.

The condition of the labor market offered more cause for concern. Although the unemployment rate edged down to 4.3% in January, annual benchmark revisions from the Bureau of Labor Statistics revealed a considerably weaker jobs picture. The economy added only 181,000 jobs throughout all of 2025, equating to approximately 15,000 per month.

This has prompted some economists to describe the current environment as one of "jobless growth"—a scenario in which the economy expands but job creation fails to keep pace. The divergence between GDP growth and employment has been widening since mid-2022, raising questions about the depth and quality of the current expansion.

International stocks and small caps emerged as leaders

Among the most notable developments in February was the continued outperformance of asset classes beyond U.S. large-cap equities. International developed markets climbed nearly 5% for the month, while emerging markets added over 5%. U.S. small caps recorded their strongest monthly performance since August, with the Russell 2000 surging roughly 5% year-to-date, well ahead of the S&P 500.

This broadening of market performance carries meaningful implications for diversified investors. Following several years in which a handful of large U.S. technology companies drove the bulk of market returns, the shift toward international equities, small caps, and cyclical sectors indicates that investors are identifying opportunities across a wider range of assets. A softer dollar earlier in the year also contributed to enhanced international returns when translated back into U.S. dollar terms.

Precious metals continued their impressive run, with gold and silver posting gains of 6.8% and 8.1%, respectively. These advances reflect a combination of geopolitical uncertainty, sustained central bank buying, and growing concerns about fiscal deficits. While precious metals can serve a role in diversified portfolios, January’s sharp reversal is a timely reminder that they are subject to meaningful price swings.

A major geopolitical development unfolded at the close of February as U.S.-Iran tensions escalated sharply following military strikes across the Middle East and reports surrounding the death of Iran’s supreme leader, Ali Khamenei. While the situation continues to evolve and geopolitical uncertainty can create market anxiety, history consistently demonstrates that staying invested has proven to be the most effective approach during such periods.

The bottom line? February’s weakness in U.S. equities was offset by gains in international markets, small caps, and bonds. While AI developments and trade policy uncertainty are likely to remain in focus, the broadening of market leadership across asset classes is an encouraging sign for long-term investors.