May proved to be a rewarding month for investors, as major indices climbed to new all-time highs despite headwinds in the bond market stemming from inflation concerns. The S&P 500 crossed the 7,500 mark for the first time, buoyed by persistent strength in technology stocks. Meanwhile, long-term interest rates surged to levels not seen in nearly two decades before pulling back later in the month as oil prices eased. Optimism around a potential peace deal in Iran also provided some support to markets, though the situation remains fluid.

May also brought the first Federal Reserve leadership change since 2018, as Kevin Warsh was sworn in as the new Fed Chair. While transitions at the top of the Fed naturally prompt questions about monetary policy direction, history demonstrates that markets and the broader economy have performed well under a wide range of Fed leaders. For long-term investors, the recent equity market strength is encouraging, though maintaining a balanced portfolio remains essential for navigating all phases of the market cycle.

Key Market and Economic Drivers in May

• The S&P 500, Nasdaq, and Dow Jones Industrial Average posted monthly gains of 5.1%, 8.4%, and 2.8%, respectively. All three major U.S. indices closed the month at record levels.

• Market volatility, as measured by the CBOE VIX index, declined over the course of the month, finishing May at 15.32.

• International developed markets delivered a return of 2.6% based on the MSCI EAFE Index in U.S. dollar terms, while emerging markets returned 9.5% based on the MSCI EM Index.

• The 30-year Treasury yield reached 5.18%, its highest point in nearly two decades, before ending the month below 5%. The 10-year Treasury yield rose to 4.4%. The Bloomberg U.S. Aggregate Bond Index returned 0.3% for the month.

• Oil prices declined, with Brent crude closing at approximately $92 per barrel and WTI at $88.

• Gold ended the month slightly lower at $4,539 per ounce. The U.S. Dollar Index stood at 98.94, also down only slightly.

• First quarter real GDP was revised lower from 2.0% quarter-over-quarter to 1.6%. April inflation showed headline CPI at 3.8% year-over-year and core CPI at 2.8%.

Long-term interest rates climbed sharply before pulling back late in the month

One of the most consequential developments in May was the sharp movement in interest rates. The 30-year U.S. Treasury yield reached its highest level in nearly two decades during the month, before settling back below 5%.

1

The 10-year and 2-year yields also moved higher as expectations grew that interest rates would remain elevated for an extended period. Markets now anticipate at least one rate hike from the Fed by mid-2027 in response to persistent inflation concerns.

This dynamic was driven by both the Consumer Price Index and Producer Price Index reports coming in above expectations, largely due to energy prices. Rising inflation tends to push interest rates higher, as investors demand greater compensation when the purchasing power of each dollar is eroding. Some economists worry that if fuel prices remain elevated, inflation could spread more broadly across goods and services. Gasoline prices have eased somewhat to around $4.30 per gallon on average nationally, but that is still roughly $1.50 higher than before the war in Iran.

2

Higher interest rates carry wide-ranging implications for both the economy and financial markets, particularly when they are driven by inflation. For consumers, the impact is felt directly through increased borrowing costs, including personal loans and mortgage rates. Businesses face similar pressures, as the cost of financing operations and funding growth rises alongside interest rates.

In financial markets, higher rates reduce the present value of future cash flows, which can weigh on asset prices. At the same time, higher yields mean that bonds are now generating more meaningful income than they have in many years, which can benefit diversified portfolios over time. It is also worth maintaining perspective: markets have moved in both directions multiple times this year as expectations around a peace deal have shifted. Interest rates have also proven difficult to forecast over recent years, and while they remain elevated today, they are still well below the levels many feared when inflation was running hotter and the Fed was in the midst of raising rates.

Equity markets continue to set new all-time highs

Despite the headwinds posed by higher interest rates, the stock market has continued to reach new record levels. The S&P 500 surpassed 7,500 for the first time in May, and there have been 22 all-time highs recorded this year through the end of the month.

3

While the Magnificent 7 and other large technology stocks have remained important contributors to market gains, the rally has been broader than in some previous years.

This favorable market environment has generated considerable interest in anticipated IPOs from companies such as SpaceX, Anthropic, OpenAI, and others. These firms have grown primarily through private investment, reflecting a broader trend over the past two decades of companies staying private for longer. While the immediate price movements following an IPO tend to attract significant attention, the longer-term significance lies in the fact that IPOs expand the investment opportunity set for all investors. Looking at today's major technology companies, it is not their IPOs that stand out most, but rather the value they have created over the decades since going public.

The fact that major indices frequently reach new all-time highs during a bull market is not unusual. Over long periods, markets have historically trended upward, meaning that indices often spend considerable time near record levels. What matters more than any single index level is whether the underlying fundamentals remain sound. Corporate earnings have continued to grow at a healthy pace, with consensus estimates pointing to further expansion in the year ahead.

4

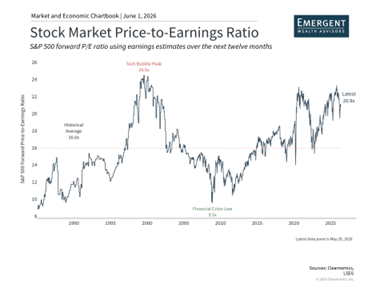

Strong earnings growth has helped keep valuations relatively stable even as the market has climbed to new highs. The S&P 500 price-to-earnings ratio is currently hovering around 20.9x, within the range observed over the past several years. That said, these valuations remain well above long-term historical averages. While elevated valuations do not necessarily predict near-term market direction, they are an important factor to consider when constructing portfolios for the long run. Maintaining diversification across sectors, market capitalizations, and investment styles can help investors manage risk while still participating in market gains.

Kevin Warsh takes the helm at the Federal Reserve

Kevin Warsh was sworn in as the new Chair of the Federal Reserve in May, succeeding Jerome Powell. Warsh previously served on the Fed's Board of Governors during the 2008 global financial crisis and is considered a known quantity by markets given his experience in monetary policy and financial markets.

Fed leadership transitions are intentionally infrequent, and they naturally generate questions about the policy path in the years ahead. Warsh is widely regarded as a reformer, which introduces some additional uncertainty around how monetary policy will be conducted under his leadership. In his recent Senate testimony, Warsh emphasized that monetary policy independence is essential and that policymakers must act in the nation's interest. He has also signaled a preference for a more focused central bank, with views that have historically leaned toward managing inflation risks.

Regardless of the institutional reforms Warsh may pursue, the Fed faces a genuinely challenging economic backdrop. The overall economy remains healthy, but inflation has picked up in recent months while the labor market has sent mixed signals. Supporting employment would typically call for lower interest rates, while bringing inflation under control would point toward tighter financial conditions. This difficult balancing act has led markets to shift from pricing in further rate cuts to now expecting at least one rate hike.

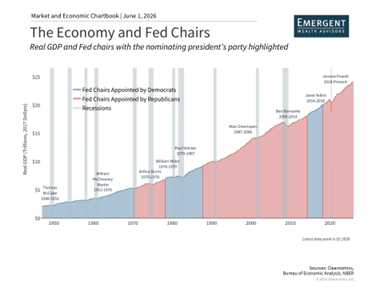

For investors, history offers an important reminder: the economy has expanded across the tenures of many different Fed chairs, regardless of the political environment or policy approach in place. Earnings growth, productivity, demographics, and innovation are ultimately the most powerful drivers of long-run investment returns. Leadership changes at the Fed can introduce near-term uncertainty, but they rarely alter these foundational long-term forces.

The bottom line? May delivered new milestones for equity markets, extending a strong run for investors. Although headlines surrounding inflation, the incoming Fed Chair, and geopolitical developments are likely to keep uncertainty elevated, the most effective approach for investors remains a focus on their long-term financial goals.

Emergent Wealth Advisors offers personalized wealth management and financial planning services to help individuals and families build, protect, and grow their financial future. Their advisors provide guidance in areas such as investment management, retirement planning, and long-term financial strategy, all tailored to each client’s specific goals and life stage. Through a thoughtful, client-focused approach, they help simplify complex financial decisions while creating a clear path toward lasting financial security and legacy planning. To learn more about how Emergent Wealth Advisors can support your financial goals, click here. If you are located in the Nashville area, click here.