For long-term investors, economic health matters significantly because it influences both portfolios and financial planning outcomes. Recent data has produced conflicting signals, creating uncertainty about the current economic landscape for some market participants.

Yet drawing conclusions from isolated data points can be misleading, much like a physician wouldn't diagnose based solely on one measurement. Blood pressure and heart rate each contribute to an overall health assessment, and what's considered normal varies among individuals. The same principle applies to economic indicators: employment figures, inflation metrics, and GDP collectively paint a complete picture. These conditions evolve throughout business cycles, and various economic environments can all support investment objectives and financial goals.

Current headline metrics appear largely favorable: economic growth exceeds forecasts, price increases are moderating, and joblessness stays low relative to historical norms. Yet employment data reveals added complexity. Though recent monthly readings proved encouraging, actual hiring throughout the past year turned out considerably weaker than initial estimates suggested. For those investing with long horizons, what matters most is comprehending how these figures interconnect to form a complete view, rather than responding to individual reports.

Employment markets are experiencing a pivotal shift

Interpreting labor market conditions has proven difficult in recent months due to government shutdowns that postponed data releases, adverse weather conditions, and various other disruptions. For workers and job seekers, the most significant development involves the changing relationship between available positions and those seeking employment.

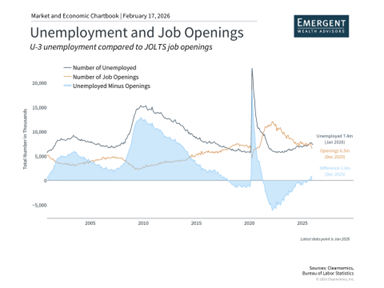

The chart above illustrates how the post-pandemic era featured multiple years where job openings exceeded the number of unemployed workers. This metric remained above one from mid-2021 through last summer, peaking at two available positions for every job seeker in 2022. Currently, approximately 7.4 million Americans are unemployed while only 6.5 million job openings exist, representing the lowest number of unfilled roles since late 2020.

Nevertheless, January's employment report delivered encouraging results, revealing that 130,000 positions were added that month, almost twice economists' projections. Healthcare, social assistance, and construction sectors accounted for many of these gains. The jobless rate decreased to 4.3% from 4.4%, remaining near historically low territory. Viewed independently, this data might indicate a rebounding labor market.

Despite these favorable figures, the overall trajectory has been more difficult. The Bureau of Labor Statistics released their yearly revisions, which incorporate more precise information than initially available for each monthly report. These revisions revealed that only 181,000 positions were created during 2025, averaging roughly 15,000 monthly—the weakest annual figure since 2020. For perspective, healthy employment growth typically measures in the millions annually before these adjustments.

How has the overall jobless rate remained relatively subdued despite slower hiring? Demographics and immigration patterns provide partial explanation. The Census Bureau recently documented a historic reduction in net international migration, declining from approximately 2.7 million in 2024 to about 1.3 million in 2025, with additional decreases anticipated. Furthermore, an aging population and reduced workforce participation translate to fewer people joining the labor force. Put differently, both labor supply and demand are moderating, helping prevent unemployment from climbing.

Employment, price pressures, and overall economic conditions

Market participants monitor employment conditions closely because they represent tangible economic activity in ways many other indicators don't. Employment directly influences household earnings, consumer sentiment, and purchasing behavior. Since consumer expenditures comprise over two-thirds of U.S. GDP, labor market developments ultimately affect the broader economy.

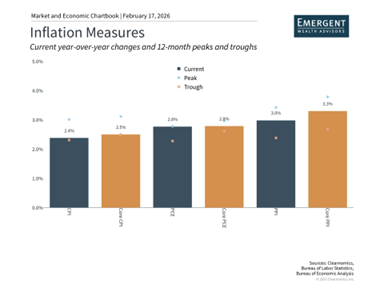

Yet employment represents just one component of the economic picture. Additional metrics, particularly inflation readings, suggest a more optimistic interpretation. Until recently, rising prices posed the greatest challenge for both investors and policymakers. Recent data indicates the Consumer Price Index increased just 2.4% over the past year, while core inflation, excluding food and energy costs, slowed to 2.5%, marking the lowest level in nearly five years. One "supercore" inflation measure, which also excludes shelter expenses, rose only 2.1% over the trailing twelve months.

This consistent moderation moves the Fed nearer to its 2% objective and indicates that inflationary forces continue diminishing. Certainly, elevated prices still burden many households and retirees since decelerating inflation doesn't mean prices actually decrease. Nonetheless, the containment of price pressures benefits both the economy and investment portfolios, given that inflation can prove problematic for equities and fixed income alike.

Portfolio implications of the current economic landscape

For investment portfolios, today's economic conditions appear cautiously favorable. The pairing of consistent growth, moderating inflation, and an easing labor market can produce a "Goldilocks" scenario that avoids extremes. This environment can support both equities and fixed income, particularly if it contributes to maintaining low interest rates. Markets responded to recent employment and inflation releases with declining interest rates across maturities, with the 10-year Treasury yield now just above 4%.

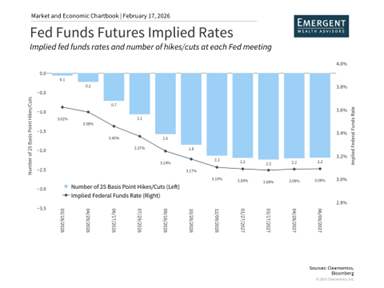

These data releases also influence Fed policy expectations and heighten the probability of rate reductions later this year. Currently, market-based indicators suggest at least two rate cuts this year, and the potential for a new Fed chair appointed by President Trump adds to this likelihood.

Should rates continue declining, portfolios benefit through reduced business borrowing costs and increased present value of future corporate profits. Outstanding bonds also typically appreciate when rates fall. Even without further rate declines, bonds continue offering appealing yields and can provide stability for long-term investors. Meanwhile, corporate profits keep expanding, representing one of the principal factors underpinning broader market performance over the past year.

The bottom line? Employment conditions are moderating while the overall economy remains sound. For investors, this nuanced environment supports maintaining balance and emphasizes the value of long-term perspective regarding portfolios and financial planning.

Emergent Wealth Advisors provides personalized wealth management and financial planning services designed to help individuals and families make confident decisions about their financial future. Their team offers comprehensive guidance, including investment and portfolio management, retirement planning, and ongoing financial planning strategies tailored to each client’s unique goals and life circumstances. By combining expert advice with a collaborative approach, they help clients simplify complex financial decisions and align their wealth with long-term goals, including retirement, tax planning, and legacy planning. For more information about how Emergent Wealth Advisors can help, please click here. For those in the Nashville area, click here.